Cash flow forecasting helps small businesses plan ahead by tracking the money expected to come in and go out of the business over a set period of time. A clear cash flow forecast can help you spot potential shortfalls early, manage day-to-day costs, and make more informed business decisions.

Even profitable businesses can run into cash flow problems if money is going out faster than it’s coming in. Late customer payments, rising overheads, seasonal dips, or unexpected expenses can all put pressure on your finances if they are not planned for properly.

In this guide, we’ll explain what a cash flow forecast is, what should be included in one, how to forecast cash flow effectively, and some of the most common mistakes small businesses make when managing cash flow.

What is a cash flow forecast?

A cash flow forecast is a financial plan that estimates how much money will come into your business and how much will go out over a set period of time.

It helps businesses understand whether they are likely to have enough cash available to cover day-to-day costs, upcoming bills, wages, supplier payments, and other financial commitments.

A cash flow forecast is usually broken down weekly or monthly and updated regularly as your business changes.

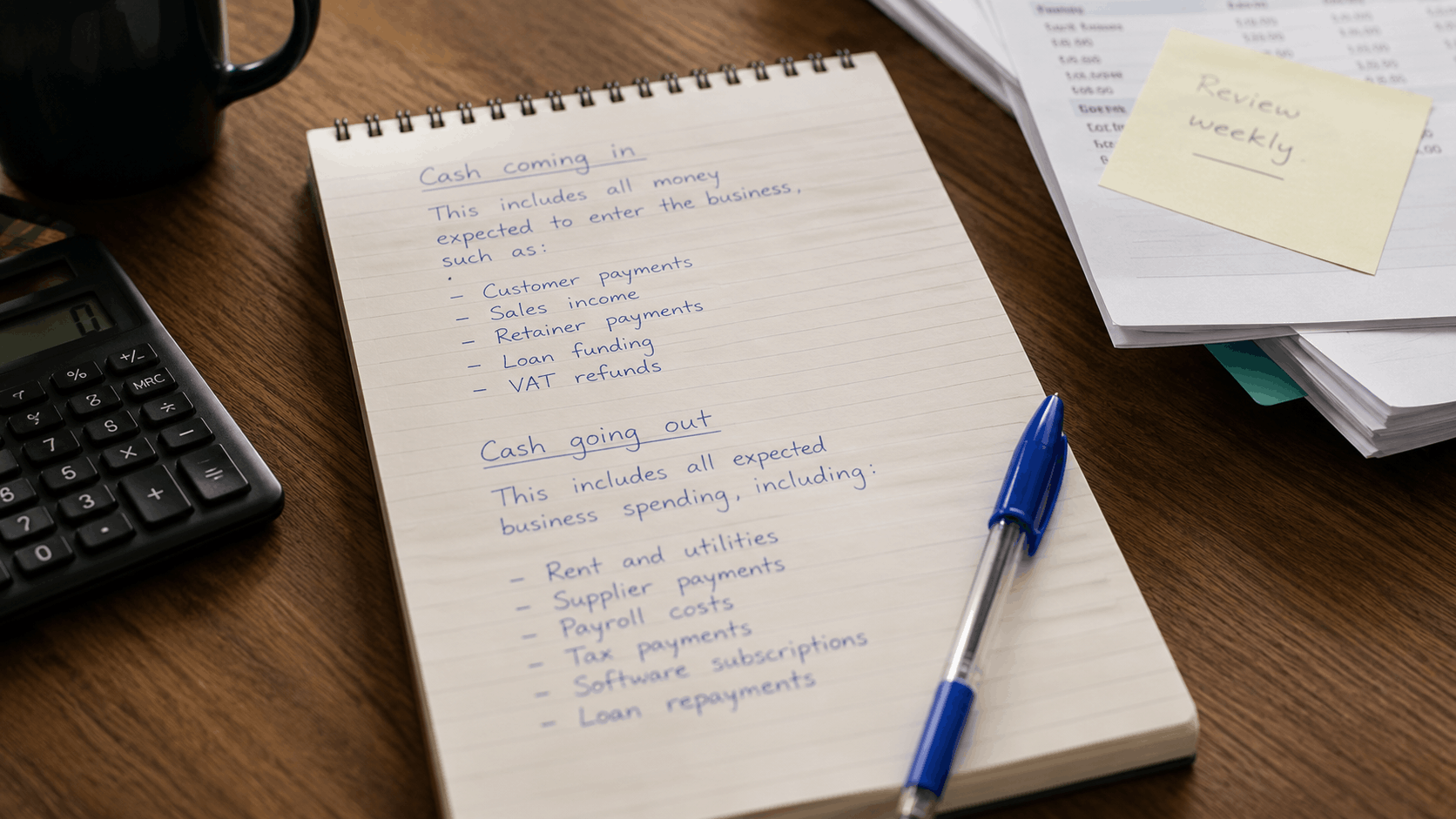

Cash coming in

This includes all money expected to enter the business, such as:

- Customer payments

- Sales income

- Retainer payments

- Loan funding

- VAT refunds

Cash going out

This includes all expected business spending, including:

- Rent and utilities

- Supplier payments

- Payroll costs

- Tax payments

- Software subscriptions

- Loan repayments

Profit vs cash flow: what’s the difference?

Profit and cash flow are often confused, but they are not the same thing.

A business can be profitable on paper while still struggling with cash flow. For example, you may have completed work and issued invoices, but if customers have not paid yet, the cash is not actually in your bank account.

Cash flow forecasting focuses on when money physically enters and leaves the business, helping you plan ahead and avoid shortfalls.

Why cash flow forecasting is important for small businesses

Cash flow forecasting gives small businesses a clearer picture of their financial position and helps them plan ahead with more confidence. Rather than reacting to problems as they happen, a good forecast allows you to spot potential issues early and make informed decisions before they become bigger problems.

For many businesses, cash flow is one of the biggest day-to-day challenges. Even when sales are strong, poor cash flow management can quickly put pressure on operations if money is not coming in at the right time.

Avoiding cash shortages

One of the biggest benefits of cash flow forecasting is identifying periods where cash may become tight. This gives you time to take action, whether that means chasing overdue invoices, reducing spending, or adjusting payment schedules with suppliers.

Without a forecast, cash shortages often come as a surprise.

Planning for VAT and tax bills

Tax payments can catch businesses out if they are not planned for properly. A cash flow forecast helps you prepare for upcoming liabilities such as:

- VAT payments

- Corporation Tax

- PAYE and National Insurance

- Self Assessment tax bills

Building these costs into your forecast reduces the risk of last-minute pressure when payment deadlines arrive.

Managing seasonal dips in revenue

Many small businesses experience quieter periods throughout the year. Retail businesses may rely heavily on Christmas trading, while construction or hospitality businesses may see fluctuations during certain seasons.

Cash flow forecasting helps you prepare for these slower periods by understanding when income is likely to dip and ensuring there is enough cash available to cover ongoing costs.

Supporting growth decisions

A strong cash flow forecast can also support business growth. It helps you assess whether the business can comfortably afford things such as:

- Hiring new staff

- Purchasing equipment

- Expanding premises

- Increasing marketing spend

- Taking on larger projects

This makes it easier to grow sustainably without putting unnecessary strain on cash flow.

Improving financial confidence

Having a clearer understanding of your cash position makes it easier to make decisions with confidence. Instead of relying on guesswork or checking your bank balance day by day, you have a forward-looking view of your finances and a better understanding of what’s coming next.

What should be included in a cash flow forecast?

A cash flow forecast should include all expected money coming into and leaving your business over a set period of time. The more accurate and realistic your forecast is, the more useful it becomes when making financial decisions.

Most small businesses create forecasts monthly, although some may choose to review them weekly if cash flow is particularly tight or unpredictable.

Below are the main areas you should include in your forecast.

Sales and customer income

Start by estimating the money expected to come into the business.

This may include:

- Customer payments

- Invoice due dates

- Recurring monthly income

- Retainer agreements

- One-off projects or contracts

- Loan funding or investment

When forecasting income, it’s important to focus on when money is actually expected to arrive in your account, not simply when an invoice is raised.

Operating costs and overheads

Your forecast should also include the regular day-to-day running costs of the business.

Common overheads include:

- Rent or office costs

- Utilities and phone bills

- Software subscriptions

- Insurance

- Marketing and advertising

- Professional fees

These fixed costs are often predictable, making them easier to build into a monthly cash flow forecast.

Payroll and staffing costs

Staffing is one of the largest expenses for many small businesses, so it should always be included in your forecast.

This may include:

- Wages and salaries

- Employer National Insurance

- Pension contributions

- Freelancers or subcontractors

- Staff bonuses or overtime

Including these costs helps ensure there is enough cash available to meet payroll commitments each month.

Tax liabilities

Tax is one of the most commonly overlooked areas of cash flow forecasting, particularly for growing businesses.

Your forecast should account for upcoming liabilities such as:

- VAT payments

- Corporation Tax

- PAYE and National Insurance

- Self Assessment tax payments

Planning ahead for tax bills can help avoid unnecessary financial pressure when deadlines approach.

Loan repayments and finance commitments

If your business has borrowed money or uses finance agreements, these repayments should be built into your forecast.

This could include:

- Business loans

- Asset finance agreements

- Credit card repayments

- Equipment leasing

Including finance commitments gives you a more accurate picture of your available cash position each month.

Stock and supplier payments

Businesses that rely on stock or materials should factor supplier costs into their forecast carefully.

This is especially important for:

- Retail businesses

- Ecommerce companies

- Hospitality businesses

- Construction firms

Changes in supplier pricing, seasonal demand, or large stock purchases can all have a major impact on cash flow.

Large one-off expenses

A good cash flow forecast should also include any significant one-off costs that may arise during the year.

Examples could include:

- Equipment purchases

- Vehicle purchases

- Office relocations

- Renovations or refurbishments

- Large software or technology investments

These expenses can create sudden pressure on cash flow if they are not planned for in advance.

How to forecast cash flow effectively

Creating a cash flow forecast does not need to be overly complicated. The goal is to build a realistic picture of the money expected to move in and out of your business over the coming weeks or months.

A good forecast helps you plan ahead, manage spending more confidently, and reduce the risk of unexpected cash flow problems.

Start with your current bank position

The first step is understanding how much cash your business currently has available.

This is known as your opening balance and forms the starting point for your forecast. Usually, this will include:

- Your business bank account balance

- Any cash reserves available

- Short-term accessible funds

Starting with an accurate opening balance gives you a clearer foundation for forecasting future cash flow.

Estimate your monthly income realistically

Next, estimate the income you expect the business to receive each month.

This could include:

- Customer payments

- Recurring contracts or retainers

- Expected invoice payments

- Seasonal sales patterns

It’s important to be realistic when forecasting revenue. Overestimating income can quickly make a forecast unreliable, particularly if customers pay late or sales fluctuate.

Where possible, base your figures on:

- Previous sales performance

- Existing contracts

- Confirmed orders

- Historical trends

Add your fixed and variable costs

Once projected income has been added, include all expected business expenses.

These are usually split into two categories:

Fixed costs

Costs that stay relatively consistent each month, such as:

- Rent

- Salaries

- Insurance

- Software subscriptions

Variable costs

Costs that can increase or decrease depending on business activity, such as:

- Stock purchases

- Utility bills

- Marketing spend

- Delivery costs

Including both fixed and variable expenses gives a more accurate view of your future cash position.

Forecast month-by-month

Most businesses create a monthly cash flow forecast to track how cash is expected to change over time.

Breaking the forecast down month-by-month makes it easier to:

- Identify quieter periods

- Plan for large payments

- Monitor growth

- Spot potential shortfalls early

Many businesses use rolling monthly forecasts, where each month is reviewed and updated as new information becomes available.

Review and update regularly

A cash flow forecast should not be treated as a one-off exercise. Your business finances will change throughout the year, so your forecast should evolve alongside them.

Reviewing your forecast regularly allows you to:

- Adjust for changes in revenue

- Update costs and supplier pricing

- Account for delayed payments

- Improve forecasting accuracy over time

The more regularly a forecast is reviewed, the more useful it becomes as a decision-making tool.

Cash flow forecasting for startups

Cash flow forecasting is particularly important for startups, where income can be less predictable and upfront costs are often much higher in the early stages of growth.

Many startups fail not because the business idea is poor, but because they run out of cash before the business becomes financially stable. Having a clear forecast helps startup owners understand what the business can realistically afford and when additional funding or cost reductions may be needed.

Why startups often struggle with cash flow

Startups typically face more cash flow pressure than established businesses because they are building revenue while already covering ongoing costs.

Common challenges include:

- Irregular or unpredictable income

- High upfront setup costs

- Customers paying invoices late

- Investing heavily in growth early on

- Limited cash reserves

In many cases, expenses begin long before revenue becomes consistent, which is why forecasting cash flow early can make a significant difference.

Common startup costs to plan for

When creating a startup cash flow forecast, it’s important to include both expected and overlooked costs.

This may include:

- Software and subscriptions

- Website and marketing costs

- Equipment and technology

- Recruitment and payroll

- Insurance and professional fees

- Tax liabilities and VAT

Including these costs early helps create a more realistic financial plan and reduces the risk of unexpected pressure later on.

Why conservative forecasting matters

One of the biggest mistakes startups make is overestimating how quickly revenue will grow.

While optimism is important when building a business, cash flow forecasting works best when figures are realistic and cautious. Conservative forecasting gives you more flexibility if sales take longer than expected or costs increase unexpectedly.

Building buffer room into your forecast can help you:

- Manage quieter periods more comfortably

- Prepare for delayed customer payments

- Handle unexpected expenses

- Reduce financial stress during growth

A cautious forecast often creates a more stable foundation for long-term business growth.

Common cash flow forecasting mistakes

Cash flow forecasting can be a valuable tool for small businesses, but only if the figures are realistic and regularly reviewed. Even small forecasting mistakes can create problems later on, particularly if costs are underestimated or income is expected too early.

Below are some of the most common cash flow forecasting mistakes businesses make and how to avoid them.

Confusing profit with cash flow

One of the biggest misunderstandings in business finance is assuming that profit automatically means healthy cash flow.

A business may appear profitable on paper while still struggling financially if customer payments have not yet been received. Cash flow forecasting focuses on when money actually enters and leaves the business, not simply when invoices are raised or sales are made.

Understanding this difference is essential for building an accurate forecast.

Forgetting annual or quarterly costs

Some business costs do not appear every month, which makes them easy to overlook when forecasting cash flow.

This may include:

- Insurance renewals

- VAT payments

- Corporation Tax

- Software renewals

- Equipment servicing

- Annual memberships or subscriptions

Missing these larger periodic costs can create unexpected pressure on cash flow later in the year.

Ignoring late payments

Many businesses forecast income based on invoice dates rather than realistic payment dates.

In reality, customers do not always pay on time. If late payments are not considered within your forecast, your projected cash position may look far healthier than it actually is.

Building realistic payment timelines into your forecast can help create a more accurate picture of available cash.

Being overly optimistic with sales forecasts

It can be tempting to base forecasts on ideal sales targets or expected growth, particularly during busy periods or when expanding the business.

However, overly optimistic forecasting can quickly become misleading if sales fall short or projects are delayed.

Cash flow forecasts tend to work best when they are based on:

- Existing customers

- Historical performance

- Confirmed work

- Realistic growth expectations

A cautious forecast usually provides more flexibility and stability.

Not updating the forecast regularly

A cash flow forecast should be reviewed and updated regularly as the business changes.

Costs may increase, customer payments may slow down, or new opportunities may arise throughout the year. A forecast that is never updated can quickly become outdated and far less useful.

Reviewing your forecast monthly helps keep figures accurate and improves decision-making over time.

Tools and templates for managing cash flow

Managing cash flow does not always require complicated software or detailed financial systems. Many small businesses start with simple spreadsheets before moving onto more advanced forecasting tools as the business grows.

The most important thing is having a system that helps you regularly track income, expenses, and future financial commitments.

Spreadsheet templates

For many small businesses and startups, spreadsheet templates are one of the simplest ways to begin cash flow forecasting.

Tools such as:

- Microsoft Excel

- Google Sheets

can be used to create a basic cash flow projection template showing:

- Opening balance

- Expected income

- Expected expenses

- Closing balance

Spreadsheet forecasting can work well for businesses with relatively straightforward finances and gives owners more control over adjusting figures manually.

Google Sheets can also be useful for collaborative forecasting, allowing multiple people within a business to review and update forecasts in real time.

Info box suggestion:

What should a simple cash flow projection template include?

A basic cash flow template should usually track:

- Opening cash balance

- Money coming in

- Money going out

- Tax liabilities

- Loan repayments

- Closing cash balance

Even a simple monthly template can provide valuable visibility over your finances.

Accounting software with forecasting tools

As businesses grow, accounting software can make cash flow forecasting faster, more accurate, and easier to maintain.

Many platforms now include built-in forecasting and reporting features, including:

- Xero

- QuickBooks

- FreeAgent

These tools can often connect directly to your bank accounts and accounting records, helping automate parts of the forecasting process and reduce manual input.

Accounting software may also help businesses:

- Monitor cash flow in real time

- Track overdue invoices

- Prepare for VAT and tax payments

- Generate financial reports more efficiently

When to get professional support

While some businesses can manage forecasting internally, professional support can become valuable as finances become more complex.

This is particularly useful for:

- Growing businesses

- Businesses experiencing cash flow pressure

- Companies applying for finance or investment

- Businesses planning expansion

Professional cash flow forecasting can help provide clearer financial visibility, improve planning, and support more informed business decisions.

Need help with cash flow forecasting?

Cash flow forecasting can provide valuable insight into the financial health of your business, but it works best when the figures are accurate, regularly reviewed, and based on realistic expectations.

At Ryans, we support small businesses with practical cash flow forecasting, clear financial reporting, and ongoing business planning guidance. Whether you need help understanding your cash position, preparing for growth, or planning for upcoming tax liabilities, we can help you build a clearer picture of your finances and make more informed business decisions.

If you would like support with cash flow forecasting or wider financial planning, our team is always happy to help.